Internationalization is a major strategic component of most business firms’ activities (Meilin, 1992), and key models of internationalization tend to describe it as taking place gradually and in distinct stages (Boisot and Meyer, 2008; Johanson & Vahlne, 1990; Meilin, 1992; Vernon, 1966). During their internationalization process, firms shift progressively from low involvement (e.g., exporting) to higher forms of involvement such as FDI in entering foreign markets (Zhao, Luo, & Suh, 2004, Boisot and Meyer, 2008). Arbitrage across borders is a process that allows firms whose domestic growth is constrained by domestic transaction and operating costs to exploit the advantages of overseas locales (Boisot and Meyer, 2008). For example, firms can harness low-cost institutional assets located outside their domestic market (Boisot and Meyer, 2008).

In this case, the paper “Pandemic Arbitrage in Foreign Direct Investments: A Perspective on the Modes of Entry” assesses whether there is “pandemic arbitrage”, i.e., whether destinations coping well with the pandemic may be more favorable to the investors. It explores how, worldwide, FDI in different entry modes responds to the COVID-19 pandemic shock. Its main contribution lies in identifying the asymmetric deterring effects of COVID-19 on different types of FDI. Applying a continuous treatment difference-in-differences (DID) approach to bilateral cross-border investment data from the Orbis database between January 2019 and December 2020, the paper finds that the pandemic deters overall FDI inflows, an intuitive result, since the pandemic generates negative economic shocks, disrupts supply chains, impedes business operations, and cuts international connections, all of which discourage profit-seeking and cost-minimizing FDI. FDI of different entry modes are likely to be exposed to the pandemic shock. In particular, the paper finds that the impact of the pandemic shock on green field FDI is more pronounced than for cross-border mergers and acquisitions (M&As). Also, strong social connections and loose COVID-19 policy stringency mitigate the pandemic’s impact on FDI, especially for M&As.

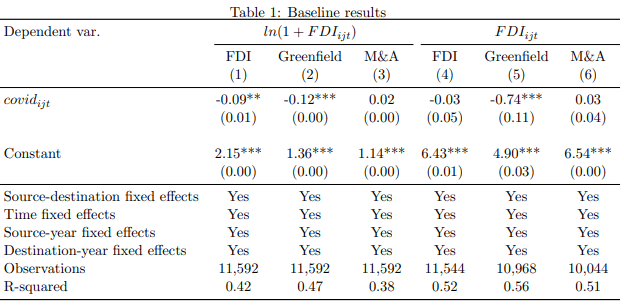

To summarize, Table 1 below shows the baseline results. A negative and statistically significant covidijt coefficient in column (1) indicates that a higher COVID-19 infection rate in the destination market relative to the source market deters FDI inflows to the destination market. In other words, FDI moves to destination markets less affected by the pandemic (or with better pandemic management). The Covidijt coefficient value indicates that a one percentage point increase in the new infection rate in the destination market relative to that in the source market corresponds to a drop in FDI inflows by 9 percent.

Secondly, since M&As require less mobile capabilities than greenfield FDI, a social connection may substitute physical connection for M&As during the pandemic, but less so for greenfield FDI. The results from columns (1) to (3) in Table 2 shows no evidence that the social connection index (SCIij) affects the impact of COVID-19 on FDI. The authors posit that this could be because the friendship connections derived from Facebook are not business oriented. Next, common colonial history is considered as an indicator of social connection. The results reported from columns (4) to (6) of Table 2 shows covidijt x socialij coeffcient as positive and significant for M&As alone. In line with expectations, a common colonial history that represents similar culture, institution, and rule between source and destination markets only weakens M&As response to COVID-19 infections.

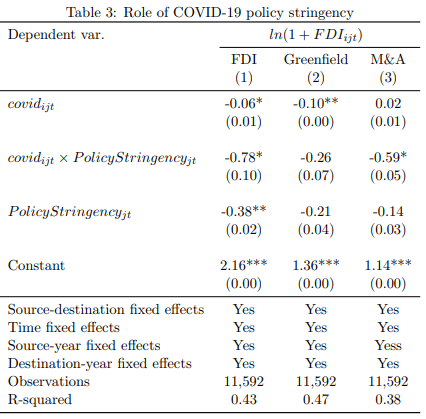

Third, the negative and significant interaction term coefficient from column (1) and (3) in Table 3 shows that COVID-19 policy stringency in the destination market strengthens the adverse impact of the pandemic on FDI inflows primarily through M&A mode of entry. From the negative and significant PolicyStringencyjt coeffcient estimate in column(1) of table 3, we also decipher that COVID-19 policy stringency directly discourages FDI.

References:

Boisot, M. and Meyer, M.W. (2008), Which Way through the Open Door? Reflections on the Internationalization of Chinese Firms. Management and Organization Review, 4: 349-365.

Cheung, P., George, A., Xie, T., Zheng, H., Zhu, Y. “Pandemic Arbitrage in Foreign Direct Investments: A Perspective on the Modes of Entry”, Research Paper #01-2022, Asia Competitiveness Institute Research Paper Series (April 2022).

Johanson, J., & Vahlne, J. 1990. The mechanism of internationalization. International Marketing Review, 7(4): 11-24.

Meilin, L. 1992. Internationalization as a Strategy Process. Strategic Management Journal, 13: 99-118.

Vernon, R. 1966. International investment and international trade in the product cycle. Quarterly Journal of Economics, 80: 190-207.

Zhao, H., Luo, Y., & Suh, T. 2004. Transaction cost determinants and ownership-based entry mode choice: A meta-analytical review. Journal of International Business Studies, 35: 524— 544.

Researchers: Paul CHEUNG, Ammu GEORGE, Taojun XIE, Huanhuan ZHENG, Yan ZHU