Summary:

In a strategic push towards fertilizer self-reliance, India has invested over ₹60,000 crore to commission six urea production plants since 2019. These investments aim to strengthen food security and reduce reliance on imports of a commodity central to India’s agricultural backbone. But do these investments truly decouple India’s fertilizer supply from global dependencies? The answer is no, as domestic production remains critically dependent on imported natural gas.

Second only to China, India’s agrarian sector is heavily dependent on fertilizers, with urea accounting for 50–60% of total consumption. Between 2018–19 and 2024–25, production growth has outpaced consumption, allowing urea imports to decline despite rising demand. This provides an important buffer in an increasingly volatile global environment. For instance, the Russia–Ukraine conflict triggered a global fertilizer shortage through trade sanctions and shipping disruptions.

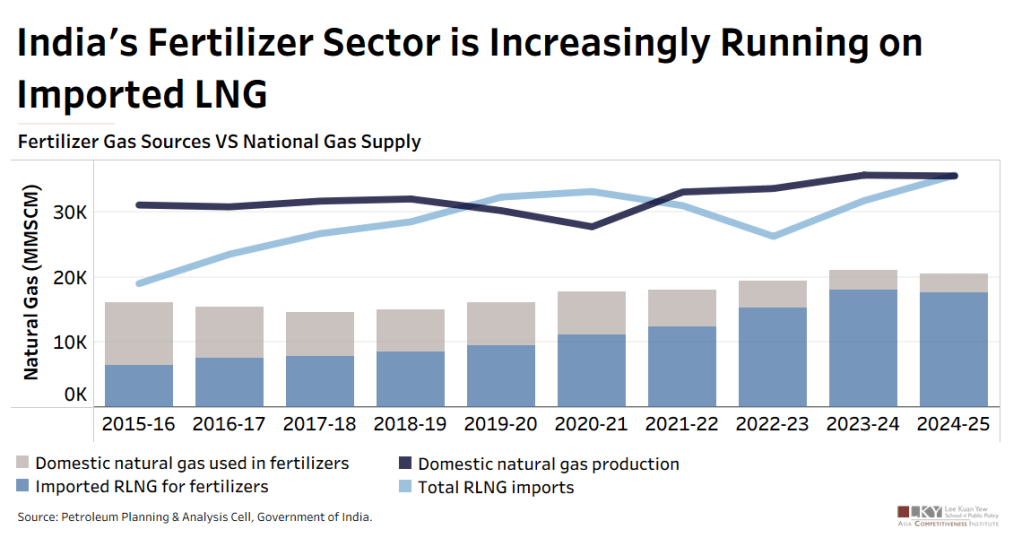

However, this falls short of fully localizing fertilizer production. Fertilizer production, particularly urea, remains heavily reliant on natural gas, and this dependence is increasingly import-driven. As seen in the figure, imported LNG used in fertilizers has risen sharply—from roughly 6,000 MMSCM in 2015–16 to over 17,000 MMSCM in 2024–25—while domestic gas usage has declined from around 10,000 MMSCM to below 3,000 MMSCM. This shift indicates that domestic fertilizer production is increasingly dependent on imported LNG.

India’s domestic gas supply has remained broadly stagnant even as overall demand rises. At the same time, this limited supply is shared across sectors—particularly power—as India targets increasing the share of natural gas in its energy mix to 15% by 2030 (from 6.4% in 2022). As a result, the fertilizer sector is increasingly pushed to substitute towards imported LNG, with R-LNG accounting for about 85% of gas used in fertilizer production in 2024–25.

This expansion in domestic fertilizer production generates important spillover effects. First, it carries significant cost implications. Domestic gas prices are capped and relatively stable, whereas imported LNG is market-linked and highly volatile. In 2024–25, domestic gas prices were capped at $6.5 per MMBtu, compared to $10.6 per MMBtu for imported LNG—before additional costs such as regasification, transportation, and taxes. Since retail prices for farmers remain heavily subsidized, these higher input costs translate into a growing fiscal burden on the government, which absorbs the difference. In some cases, producing urea domestically using expensive imported gas can even cost more than importing urea directly. The rising reliance on imported LNG in fertilizer production might further amplify this fiscal burden.

Second, there are growing supply-side vulnerabilities. India’s LNG imports remain geographically concentrated, with around 43% sourced from Qatar, 11% from the UAE, and 5% from Oman. While diversification in the US and Africa has increased, recent geopolitical developments highlight the risks of such dependence. Supply disruptions or price shocks in these regions can directly impact fertilizer production costs, with cascading effects on fiscal stability and food security.

Highlights:

1. Shallow decoupling: Domestic fertilizer production is dependent on a sharp rise in imported LNG use alongside a fall in domestic gas usage.

2. Fiscal spillovers: The increasing share of imported LNG in fertilizer production (now around 85%) reflects greater exposure to higher and more volatile input costs.

3. Geopolitical exposure: The shift from domestic gas to imported LNG in the fertilizer sector underscores rising dependence on external supply sources, increasing vulnerability of a critical sector to global supply shocks.

Article By Riddhimaa, GUPTA

Graphic By HUANG, Yijia